Introduction: Understanding Debt Collection Attorneys and Their Role in Financial Recovery

When facing debt collection issues, many Americans find themselves overwhelmed by aggressive collection tactics, confusing legal notices, and the stress of financial uncertainty. A debt collection attorney can be a powerful ally in navigating these challenges. These specialized lawyers understand the complex laws governing debt collection and can represent both creditors seeking payment and consumers defending against collection actions.

Debt collection attorneys play a crucial role in the American financial system, helping to balance the legitimate interests of creditors with the legal protections afforded to consumers. Whether you’re being pursued for unpaid debts or need assistance recovering money owed to you, understanding how these legal professionals work can significantly impact your financial outcomes.

What Is a Debt Collection Attorney?

A debt collection attorney is a legal professional who specializes in matters related to debt collection. These attorneys have specific expertise in debt collection laws, credit agreements, consumer protection regulations, and litigation procedures related to monetary claims.

Types of Debt Collection Attorneys

Debt collection attorneys generally fall into two categories:

1. Consumer-Side Attorneys: These lawyers represent individuals who are being pursued by creditors or collection agencies. They help consumers understand their rights, challenge improper collection practices, defend against lawsuits, and negotiate settlements.

2. Creditor-Side Attorneys: These attorneys represent lenders, creditors, or collection agencies seeking to recover unpaid debts. They handle legal procedures necessary to collect debts, including filing lawsuits, obtaining judgments, and pursuing post-judgment remedies like wage garnishment or property liens.

What Debt Collection Attorneys Do

The specific services provided by debt collection attorneys vary depending on whether they represent creditors or consumers:

For Consumers:

- Reviewing debt collection notices and verifying debt validity

- Stopping harassment from debt collectors

- Representing clients in debt collection lawsuits

- Negotiating debt settlements for less than the full amount

- Advising on bankruptcy options when appropriate

- Identifying violations of consumer protection laws

- Pursuing damages for illegal collection practices

For Creditors:

- Sending demand letters to debtors

- Filing and prosecuting collection lawsuits

- Obtaining judgments against debtors

- Implementing post-judgment collection strategies

- Navigating bankruptcy proceedings when debtors file

- Advising on compliance with collection regulations

When Do You Need a Debt Collection Attorney?

For Consumers Facing Collection

If you’re on the receiving end of collection efforts, certain situations strongly indicate the need for legal representation:

1. You’ve been served with a debt collection lawsuit: If you’ve received a summons and complaint, consulting with an attorney immediately is crucial. In most states, you have only 20-30 days to respond, and failure to do so can result in a default judgment against you.

2. You’re experiencing harassment from collectors: If debt collectors are calling at unreasonable hours, using abusive language, making threats, or contacting you at work after being asked to stop, an attorney can help end these illegal practices.

3. You believe the debt is invalid: If you don’t recognize the debt, believe the amount is incorrect, or think the statute of limitations has expired, an attorney can help you challenge the debt’s validity.

4. You’re facing wage garnishment or bank levies: If a creditor has already obtained a judgment and is trying to seize your assets or garnish your wages, an attorney may be able to help you protect certain exempt income and property.

5. You’re being sued for a large amount: If the debt in question is substantial, the cost of legal representation may be justified by the potential savings.

For Creditors Seeking Collection

From the creditor side, these situations typically warrant attorney involvement:

1. The debt exceeds $5,000: Many collection professionals recommend hiring an attorney when the unpaid debt is $5,000 or more, as the potential recovery justifies the legal expenses.

2. The debtor is a large company: When pursuing payment from substantial businesses with significant resources, specialized legal knowledge becomes essential.

3. Previous collection attempts have failed: If standard collection procedures haven’t yielded results, an attorney can escalate to legal action.

4. The statute of limitations is approaching: When time is running out to legally collect a debt, prompt legal action becomes necessary.

5. Complex legal issues are involved: Some collection matters involve complicated legal questions that require expert analysis.

The Legal Process of Debt Collection

Pre-Lawsuit Collection Efforts

Before litigation begins, creditors typically engage in various collection attempts:

- Internal Collection: The original creditor may try to collect through statements, letters, and phone calls.

- Third-Party Collection Agency: If internal efforts fail, the debt may be assigned to a collection agency that specializes in recovering unpaid debts.

- Debt Sale: Some creditors sell delinquent accounts to debt buyers, who then pursue collection.

- Attorney Demand Letters: Before filing suit, an attorney often sends formal demand letters requesting payment and warning of potential legal action.

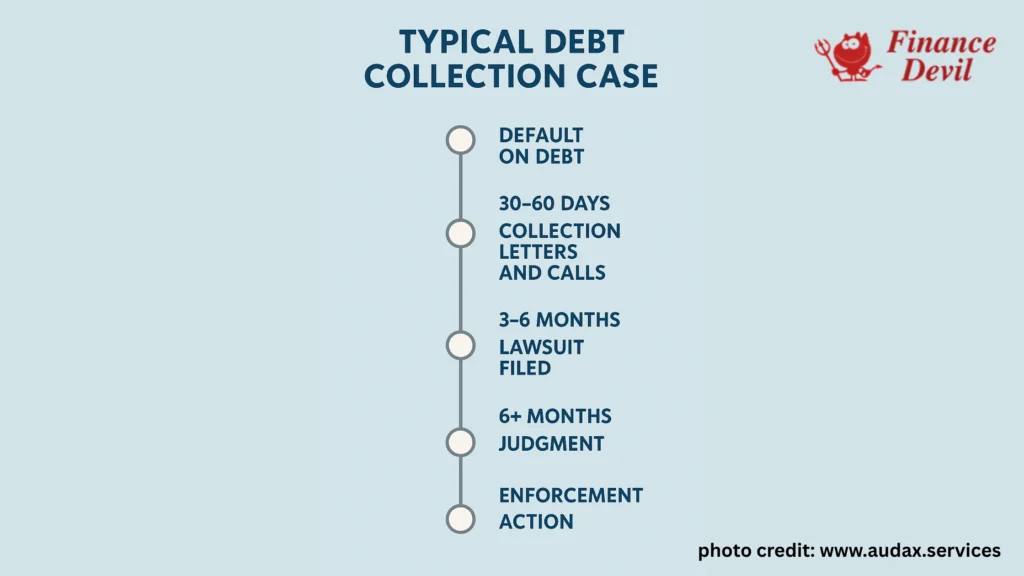

The Debt Collection Lawsuit Process

When pre-lawsuit efforts fail, the legal process typically follows these steps:

- Filing and Service: The creditor’s attorney files a complaint in court and serves it on the debtor along with a summons.

- Response Period: The debtor generally has 20-30 days (varies by state) to file a written answer to the complaint.

- Default Judgment: If the debtor fails to respond, the court may enter a default judgment in favor of the creditor.

- Discovery: If the debtor responds, both sides exchange information relevant to the case through a process called discovery.

- Motions: Either party may file motions asking the court to make decisions on specific issues before trial.

- Settlement Negotiations: Many cases settle during this phase, often with payment plans or reduced lump-sum payments.

- Trial: If no settlement is reached, the case proceeds to trial where a judge (or sometimes a jury) determines the outcome.

- Judgment: If the creditor prevails, the court enters a judgment specifying the amount owed.

- Post-Judgment Collection: With a judgment in hand, creditors can pursue various collection methods including wage garnishment, bank account levies, and property liens.

Consumer Rights and Protections in Debt Collection

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA is a federal law that prohibits debt collectors from using abusive, unfair, or deceptive practices when collecting consumer debts. Key protections include:

- Communication Restrictions: Collectors cannot contact consumers before 8 a.m. or after 9 p.m., or at work if told not to.

- Third-Party Contact Limitations: Collectors generally cannot discuss your debt with anyone except you, your spouse, or your attorney.

- Harassment Prohibition: The law forbids threats, profanity, repeated calls intended to annoy, and false statements.

- Debt Verification Rights: If you request verification of a debt in writing within 30 days of being contacted, the collector must provide proof of the debt before continuing collection efforts.

- Cease Communication Requests: You can send a written request for a collector to stop contacting you, though this doesn’t eliminate the debt.

State-Specific Protections

Many states have enacted additional consumer protections that go beyond federal requirements. For example:

- California’s Rosenthal Fair Debt Collection Practices Act applies to original creditors as well as third-party collectors.

- New York’s Consumer Credit Fairness Act shortens the statute of limitations on consumer debt and enhances documentation requirements for collectors.

- Texas Debt Collection Act provides remedies against collectors who threaten criminal prosecution for civil debts.

Statute of Limitations on Debt Collection

Each state establishes time limits for filing lawsuits to collect debts. These statutes of limitations typically range from 3 to 10 years, depending on the state and type of debt. Once this period expires, the debt becomes “time-barred,” meaning a creditor can no longer successfully sue to collect it.

However, it’s important to note:

- Making a payment or acknowledging a debt in writing can restart the statute of limitations in many states.

- Collectors can still attempt to collect time-barred debts, though they cannot threaten to sue.

- Some states require collectors to disclose when debts are time-barred.

How to Find and Choose a Debt Collection Attorney

Sources for Finding Qualified Attorneys

- State Bar Association Referral Services: Most state bar associations operate lawyer referral services that can connect you with attorneys experienced in debt collection matters.

- National Association of Consumer Advocates (NACA): For consumer-side representation, NACA maintains a directory of attorneys who specialize in consumer protection.

- Legal Aid Organizations: If you have limited income, you may qualify for free or low-cost legal assistance through legal aid societies.

- Consumer Financial Protection Bureau (CFPB): The CFPB website provides resources to help find legal assistance with debt issues.

- Online Legal Directories: Websites like Avvo, FindLaw, and Martindale-Hubbell allow you to search for attorneys by practice area and location, along with reviews and ratings.

- Personal Referrals: Recommendations from friends, family members, or other attorneys who have had positive experiences can be valuable.

What to Look for in a Debt Collection Attorney

When selecting an attorney, consider these important factors:

1. Specialization and Experience

- How much of their practice is dedicated to debt collection matters?

- How many similar cases have they handled?

- Do they typically represent consumers, creditors, or both?

2. Knowledge of Relevant Laws

- Are they familiar with both federal laws (like the FDCPA) and the specific laws of your state?

- Do they keep up with changes in debt collection regulations?

3. Communication Style

- Do they explain legal concepts clearly?

- Are they responsive to your questions?

- Do they return calls and emails promptly?

4. Fee Structure

- Do they charge hourly rates or flat fees?

- For consumer cases, do they take cases on contingency (getting paid only if you win)?

- Are payment plans available?

5. Professional Standing

- Are they in good standing with the state bar?

- Have they faced disciplinary actions?

- What do client reviews and testimonials indicate about their service?

Questions to Ask During Your Initial Consultation

Most debt collection attorneys offer free or low-cost initial consultations. Make the most of this opportunity by asking:

- What strategies would you recommend for my specific situation?

- What potential outcomes should I expect?

- How long might my case take to resolve?

- How will we communicate throughout the process?

- What documentation do you need from me?

- What are the total estimated costs for handling my case?

- Have you handled cases against this particular creditor/debt collector before?

READ ALSO: Take Control of Your Debt: A Comprehensive Guide to Strategic Debt Management

Working with a Debt Collection Attorney: What to Expect

Preparing for Your First Meeting

To make your initial consultation productive, gather these documents beforehand:

- Collection notices and letters you’ve received

- The original credit agreement or contract

- Your payment history

- Any correspondence you’ve had with the creditor or collector

- Court documents if you’ve been sued

- Records of communications (dates, times, names of representatives)

- Your credit reports

- Financial information showing your current situation

The Attorney-Client Relationship

When you hire a debt collection attorney, understanding the professional relationship helps set appropriate expectations:

1. Attorney’s Responsibilities:

- Providing legal advice based on your specific situation

- Explaining your options and their potential consequences

- Developing strategies to achieve your goals

- Representing your interests in negotiations and court proceedings

- Keeping you informed about case developments

- Maintaining confidentiality of your information

2. Your Responsibilities:

- Providing complete and accurate information

- Being truthful about your financial situation

- Promptly responding to requests for documents or information

- Making timely decisions when options are presented

- Attending scheduled meetings and court appearances

- Paying agreed-upon legal fees

Communication Protocols

Effective communication is essential for successful representation. Discuss with your attorney:

- Preferred methods of communication (phone, email, text)

- Expected response times

- How often you’ll receive case updates

- Who to contact if your attorney is unavailable

- Protocol for emergencies

Cost of Hiring a Debt Collection Attorney

Fee Structures for Consumer Representation

Attorneys who represent consumers in debt collection matters typically use these fee arrangements:

1. Contingency Fees: For cases involving violations of consumer protection laws, attorneys may take cases on contingency, meaning they only get paid if they win money for you. The fee is usually a percentage (typically 30-40%) of the recovery.

2. Hourly Rates: For debt defense cases, attorneys often charge hourly rates ranging from $150 to $350, depending on their experience and location.

3. Flat Fees: Some services, like reviewing a settlement offer or drafting a cease-communication letter, may be available for fixed fees ranging from $250 to $1,500.

4. Hybrid Arrangements: Some attorneys combine approaches, such as a reduced hourly rate plus a smaller contingency percentage if you win.

Fee Structures for Creditor Representation

When representing creditors, attorneys typically use:

1. Contingency Fees: Collection attorneys often work on contingency, taking a percentage (typically 25-40%) of amounts recovered.

2. Hourly Rates: For complex cases or when specific legal services are needed, hourly rates generally range from $200 to $400.

3. Flat Fees: Routine collection actions like drafting demand letters or filing simple lawsuits may be available for set fees.

Cost-Benefit Analysis

When deciding whether to hire an attorney, consider:

- The amount of debt involved

- The strength of your legal position

- The potential consequences of losing

- The cost of representation versus potential savings or recovery

- Non-financial benefits like reduced stress and time savings

Alternatives to Hiring a Debt Collection Attorney

Self-Representation Options

For consumers with simple cases or limited budgets, these options may be worth considering:

1. Pro Se Representation: You can represent yourself in court (called “pro se” representation). Many courts have self-help resources for people without attorneys.

2. Legal Coaching: Some attorneys offer “unbundled” services, providing guidance while you handle most aspects of your case yourself.

3. Online Resources: Websites like LawHelp.org, SelfHelpSupport.org, and court websites offer guidance on responding to collection lawsuits.

Debt Management and Settlement Companies

Non-legal options include:

1. Credit Counseling Agencies: Nonprofit organizations that can help you develop budgets and debt management plans.

2. Debt Settlement Companies: For-profit companies that negotiate with creditors to accept less than the full amount owed. Be cautious, as this industry includes many questionable operators.

3. Bankruptcy Counseling: Meeting with a bankruptcy attorney can help you understand if bankruptcy might be appropriate for your situation.

When to Choose Each Alternative

Consider these factors when deciding between attorney representation and alternatives:

- Complexity: Simple cases with clear facts may be manageable without an attorney.

- Amount at Stake: Higher debt amounts justify higher legal expenses.

- Legal Issues: Cases involving legal violations or complex defenses benefit more from attorney expertise.

- Personal Capacity: Your comfort with legal procedures and stress tolerance matter.

- Financial Resources: Your ability to afford legal fees affects your options.

Strategic Approaches to Debt Collection Cases

For Consumers Defending Against Collection

Effective defense strategies often include:

1. Challenging the Collector’s Standing

- Requesting debt validation to verify the collector has the right to collect

- Demanding documentation showing the chain of ownership if the debt has been sold

- Questioning whether the plaintiff is the real party in interest

2. Procedural Defenses

- Asserting statute of limitations has expired

- Challenging proper service of the lawsuit

- Identifying jurisdictional issues

3. Substantive Defenses

- Disputing the amount of the debt

- Demonstrating prior payment or settlement

- Identifying identity theft or mistaken identity

- Proving violation of lending or collection laws

4. Settlement Strategies

- Lump-sum settlements for less than the full amount

- Structured payment plans without additional fees

- Debt validation during the collection process

For Creditors Pursuing Collection

Effective collection strategies typically include:

1. Pre-Litigation Approaches

- Strategic timing of demand letters

- Skip-tracing to locate debtors

- Asset searches to identify collection sources

- Credit bureau reporting as leverage

2. Litigation Strategies

- Targeting debtors with documented assets or income

- Using discovery to identify hidden assets

- Pursuing prejudgment remedies when available

- Efficiently managing large volumes of similar cases

3. Post-Judgment Enforcement

- Wage garnishment procedures

- Bank account levies

- Property liens

- Judgment debtor examinations

READ ALSO: What Is Convertible Debt?

Debt Collection Lawsuits and Default Judgments

Understanding Default Judgments

A default judgment occurs when you fail to respond to a lawsuit within the required timeframe. This has serious consequences:

- The creditor wins automatically without having to prove their case

- The judgment appears on your credit report for up to 10 years

- The creditor gains powerful collection tools like wage garnishment

- You lose the opportunity to raise defenses or negotiate

According to a 2020 study by the Pew Charitable Trusts, more than 70% of debt collection lawsuits end in default judgments, often because consumers don’t know how to respond properly.

How to Avoid Default Judgments

If you’ve been served with a collection lawsuit:

- Note the deadline to respond (typically 20-30 days from service)

- Don’t ignore the paperwork, even if you believe the debt isn’t yours

- File a written answer with the court that addresses each claim

- Consult with an attorney even if you can’t afford full representation

- Consider legal aid if you qualify based on income

- Request an extension if you need more time to respond

Responding to a Collection Lawsuit

Your written response (Answer) to a collection lawsuit should:

- Address each allegation in the complaint

- Assert applicable affirmative defenses

- Be filed with the correct court within the deadline

- Be properly served on the plaintiff’s attorney

- Follow local court formatting rules

Common defenses include:

- Statute of limitations has expired

- The debt has been paid or settled

- The amount claimed is incorrect

- You are not the person who owes the debt

- The plaintiff cannot prove ownership of the debt

- The debt was discharged in bankruptcy

- The contract terms were unfair or illegal

Bankruptcy as a Solution to Debt Collection Problems

How Bankruptcy Stops Debt Collection

Filing for bankruptcy provides immediate protection through the “automatic stay,” which:

- Stops all collection calls, letters, and lawsuits

- Halts wage garnishments and bank levies

- Prevents foreclosures and repossessions (at least temporarily)

- Prohibits creditors from contacting you directly

Types of Bankruptcy for Consumers

Chapter 7 Bankruptcy:

- Often called “liquidation bankruptcy”

- Eliminates most unsecured debts like credit cards and medical bills

- Typically completed in 3-6 months

- May require surrendering non-exempt property

- Eligibility depends on income (means test)

- Remains on credit report for 10 years

Chapter 13 Bankruptcy:

- Called “reorganization bankruptcy”

- Creates 3-5 year payment plan for debts

- Allows you to keep property while paying creditors

- Good option for those with steady income

- Helps save homes from foreclosure

- Remains on credit report for 7 years

When Bankruptcy Makes Sense

Bankruptcy might be appropriate when:

- Your debts far exceed your ability to pay

- You face multiple collection lawsuits

- Your wages are being garnished

- Essential property is at risk of seizure

- You’re using credit cards to pay for necessities

- Debt stress is affecting your physical or mental health

Working with a Bankruptcy Attorney

While some consumers file bankruptcy without legal help (pro se), working with a qualified bankruptcy attorney offers significant advantages:

- Proper filing of complex forms and schedules

- Strategic timing of your filing

- Maximizing property exemptions

- Navigating means test requirements

- Representation at the meeting of creditors

- Addressing any challenges to discharge

Recent Trends and Developments in Debt Collection

Impact of COVID-19 on Debt Collection

The pandemic created significant changes in the debt collection landscape:

- Temporary moratoriums on certain collection activities

- Increased flexibility from many creditors regarding hardship programs

- Rise in medical debt due to COVID-related hospitalizations

- Growth in consumer debt as many households faced income disruption

- Court backlogs delaying debt collection litigation

- Increased use of electronic communication and virtual court proceedings

Regulatory Changes

Recent regulatory developments affecting debt collection include:

1. CFPB Debt Collection Rule: Implemented in November 2021, this rule clarifies how the FDCPA applies to modern communications like emails and text messages, limits call frequency, and requires certain disclosures.

2. State Reforms: Several states have enacted stricter debt collection regulations, including:

- New York’s Consumer Credit Fairness Act (reduces statute of limitations from 6 to 3 years)

- California’s Debt Collection Licensing Act (requires licensing of debt collectors)

- Washington’s medical debt collection restrictions

3. Student Loan Collection Changes: Federal student loan collection practices have undergone significant reform, including expanded income-driven repayment options and temporary payment pauses.

Technology in Debt Collection

Technology is transforming debt collection practices:

- AI and Machine Learning: Used to determine optimal contact times and personalize collection approaches

- Digital Communication Platforms: Allowing consumers to negotiate and make payments online

- Speech Analytics: Monitoring collector calls for compliance with regulations

- Consumer-Facing Portals: Enabling self-service options for consumers to resolve debts

- Electronic Court Filing: Streamlining the litigation process

Conclusion: Making Informed Decisions About Debt Collection Legal Matters

Navigating debt collection issues requires understanding both legal rights and practical realities. Whether you’re a consumer facing collection efforts or a creditor seeking to recover funds, knowledgeable legal representation can significantly improve your outcomes.

For consumers, a debt collection attorney can level the playing field, ensuring that collectors follow the law and that you don’t pay more than you legally owe. For creditors, skilled legal counsel can maximize recovery while maintaining compliance with increasingly complex regulations.

The decision to hire a debt collection attorney should be based on a careful assessment of your specific situation, including the amount at stake, the complexity of the legal issues involved, and your financial resources. In many cases, the value provided by expert legal guidance far exceeds the cost.

Whatever your situation, taking proactive steps rather than ignoring debt issues is almost always the better strategy. Legal problems related to debt rarely resolve themselves and often worsen with time. By understanding your options and seeking appropriate guidance, you can work toward resolving debt issues and restoring financial stability.

FAQ: Common Questions About Debt Collection Attorneys

For Consumers

Q: Can a debt collection attorney help me if I’ve already received a judgment?

A: Yes. Even after a judgment, an attorney might be able to negotiate a settlement, file a motion to vacate the judgment if proper procedures weren’t followed, or help protect exempt income and assets from collection.

Q: Will hiring an attorney make debt collectors stop contacting me?

A: Yes. Under the FDCPA, once you inform a debt collector that you’re represented by an attorney, they must communicate only with your attorney, not with you directly.

Q: How much does it cost to fight a debt collection lawsuit?

A: Costs vary widely depending on case complexity and your location. Simple cases might cost $500-1,500, while complex litigation could cost several thousand dollars. Some consumer attorneys work on contingency or offer payment plans.

Q: Can I recover attorney fees if I win my case against a debt collector?

A: Possibly. If the debt collector violated the FDCPA or similar state laws, you may be entitled to recover reasonable attorney fees and costs if you prevail.

Q: If I settle a debt, will it affect my credit score?

A: Yes, but how much depends on how the creditor reports it. A “paid in full” notation is better than “settled for less than full amount,” but both are better than “unpaid” or “charged off” status.

For Creditors

Q: How long does it typically take to collect a debt through legal channels?

A: The timeline varies greatly depending on the jurisdiction, debtor’s response, and collection strategy. Simple cases might resolve in 3-6 months, while contested matters can take a year or more.

Q: What percentage of the debt can I expect to recover?

A: Recovery rates vary widely. According to industry data, the average recovery rate for fresh debts (less than 1 year old) is about 30-35%, while older debts may yield recovery rates of 5-15%.

Q: Can I recover my attorney fees when suing to collect a debt?

A: Often yes, if your original contract with the debtor includes an attorney fee provision. Many states also have statutes allowing recovery of reasonable collection costs.

Q: Is it better to file many small lawsuits or combine claims?

A: This strategic decision depends on court filing fees, the relationship between the claims, and jurisdictional limits. Your attorney can advise on the most cost-effective approach.

Q: Should I accept a payment plan or hold out for a lump sum?

A: This depends on the debtor’s financial situation, the amount owed, and your cash flow needs. Payment plans increase the total collection period but may result in higher total recovery than a heavily discounted lump sum.

In another related article, Best Small Business Attorneys in Florida: Your Complete Guide for 2025