If you are thinking about refinancing your mortgage in 2026, one of the most consequential decisions you will make has nothing to do with which lender you choose. It is about the type of loan you refinance into. Specifically: a fixed-rate mortgage or an adjustable-rate mortgage (ARM).

The difference can translate to tens of thousands of dollars in interest over the life of your loan, or it can mean the difference between a payment that never changes and one that spikes without warning. With 30-year fixed refinance rates averaging 6.78% APR and 5/1 ARM refinance rates sitting around 6.34% APR as of early April 2026, the gap is real but narrower than many homeowners expect.

This guide breaks down both options side by side so you can make a confident, data-backed decision based on your timeline, budget, and risk tolerance.

What Is a Fixed-Rate Refinance?

A fixed-rate refinance replaces your existing mortgage with a new loan that carries one interest rate for the entire term, whether that is 10, 15, or 30 years. Your principal and interest payment never changes, making it easy to budget and plan long-term.

As of April 3, 2026, Bankrate reports the national average 30-year fixed refinance APR at 6.78%, while the 15-year fixed refinance APR averages 6.10%. According to Freddie Mac, approximately 92% of all U.S. mortgage holders have chosen fixed-rate loans, a clear signal of how much American homeowners value payment stability.

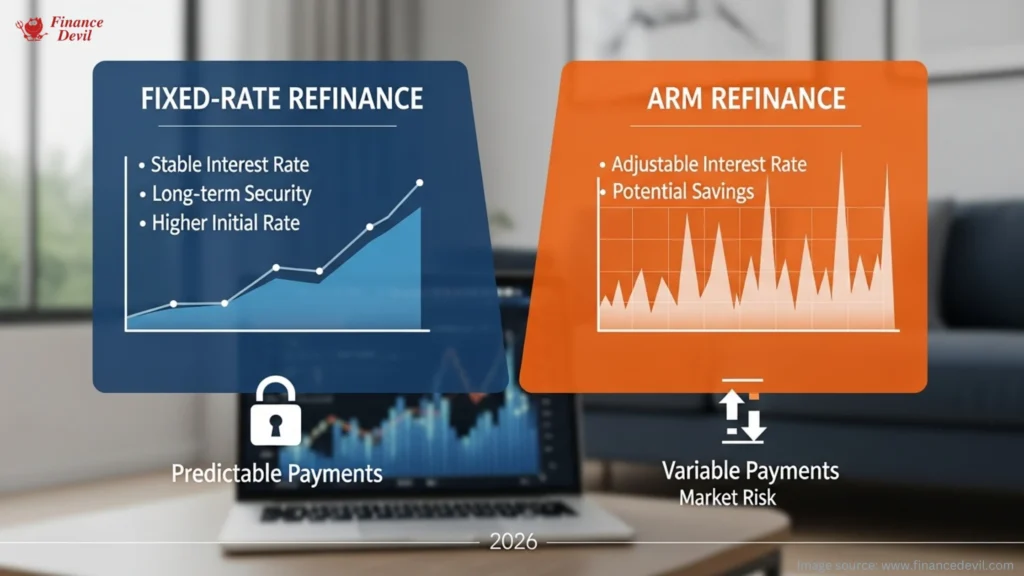

Key Advantages of a Fixed-Rate Refinance

- Predictable payments. Your principal and interest amount never changes, regardless of what happens to interest rates in the broader market.

- Protection from rate increases. If market rates rise in 2027 or 2028, you are completely insulated.

- Simpler to manage. No caps, no margin calculations, no rate adjustment notices to track.

- Ideal for long-term homeowners. If you plan to stay in your home for 10 or more years, locking in a rate now gives you lasting certainty.

Potential Drawbacks

- Higher starting rate compared to an ARM’s introductory rate.

- You pay more in the early years if you end up selling or refinancing again within a few years.

- Closing costs of 2% to 5% of the loan amount apply, same as with an ARM.

What Is an ARM Refinance?

An adjustable-rate mortgage (ARM) refinance replaces your current mortgage with a loan that has a lower fixed rate for an initial period, then adjusts periodically based on a market index such as the Secured Overnight Financing Rate (SOFR) plus a lender margin.

The most common ARM structures include the 5/1 ARM (fixed for five years, then adjusts annually), the 7/6 ARM (fixed for seven years, then adjusts every six months), and the 10/1 ARM (fixed for 10 years, then adjusts annually). As of March 24, 2026, Bankrate reported the national average 5/1 ARM refinance APR at 6.34% and the 10/1 ARM refinance APR at 6.50%.

Common ARM Structures at a Glance

| ARM Type | Fixed Period | Adjusts Every | Best For |

|---|---|---|---|

| 3/1 ARM | 3 years | Annually | Very short-term owners |

| 5/1 ARM | 5 years | Annually | Flippers or 5-yr planners |

| 5/6 ARM | 5 years | Every 6 months | Short-to-mid term stays |

| 7/1 ARM | 7 years | Annually | Mid-term owners (5-7 yrs) |

| 7/6 ARM | 7 years | Every 6 months | Mid-term with more flexibility |

| 10/1 ARM | 10 years | Annually | Longer-term but uncertain plans |

Source: Bankrate, Fortune, RefiGuide (April 2026)

Key Advantages of an ARM Refinance

- Lower initial rate. The introductory period offers a rate that is typically 0.5% to 0.8% below comparable fixed-rate loans in the current market.

- Lower early payments. Monthly savings during the fixed period can be significant on larger loan balances.

- Strategic exit potential. If you plan to sell or refinance again before the adjustment period begins, you capture the savings without any of the risk.

- Potentially easier to qualify. Some lenders apply less stringent requirements for ARMs than for fixed-rate loans.

Potential Drawbacks

- Payment shock risk if rates climb after the fixed period ends.

- Complex terms make rate-shopping harder than with fixed loans.

- Long-term costs are unpredictable and can exceed fixed-rate costs if rates rise.

- As Chase notes, ARM borrowers need a meaningful level of risk tolerance, and a clear plan for when higher payments eventually kick in.

Fixed-Rate vs. ARM Refinance: Side-by-Side Comparison

Use this table to compare the two options at a glance based on the most important decision factors for U.S. homeowners in 2026.

| Feature | Fixed-Rate Refinance | ARM Refinance |

|---|---|---|

| Interest Rate | Locked in for life of loan | Fixed intro period, then adjusts |

| Monthly Payment | Stays the same every month | May rise or fall after adjustment |

| Current Rate (30-yr) | ~6.78% APR (Apr 2026) | ~6.34% APR (5/1 ARM) |

| Best For | Long-term homeowners (7+ yrs) | Short-term owners (under 7 yrs) |

| Rate Risk | None | High after fixed period ends |

| Budgeting | Easy and predictable | Uncertain after intro period |

| Closing Costs | 2% to 5% of loan amount | 2% to 5% of loan amount |

| Rate Savings | Minimal; rate locked in | Initial savings of 0.5-0.8% |

| Risk Level | Low | Medium to High |

Sources: Bankrate (April 3, 2026), Fortune, Freddie Mac, Chase

How Much Can You Really Save With an ARM?

The honest answer in 2026 is: less than you might think. The spread between a 5/1 ARM and a 30-year fixed mortgage is currently around 0.44 to 0.80 percentage points, according to data from Bankrate and RefiGuide. Historically, ARMs offered a much larger initial discount, which made the risk easier to justify. That gap has narrowed considerably.

To put it in dollar terms: on a $400,000 loan balance, a 0.44% rate difference amounts to roughly $125 per month in initial savings with an ARM. Over five years, that is about $7,500 saved before the first adjustment occurs. But if your ARM rate climbs by even 1% after year five, you could erase those savings within two to three years of the adjustment period.

| Expert Insight“This lower rate environment is not only improving affordability for prospective homebuyers, it’s also strengthening the financial position of homeowners.”— Sam Khater, Chief Economist, Freddie Mac (February 2026). Freddie Mac PMMS |

Who Should Choose a Fixed-Rate Refinance?

A fixed-rate refinance is almost always the right choice if any of the following apply to you.

- You plan to stay in your home for seven or more years. The longer your time horizon, the more valuable rate certainty becomes. Over a decade or more, any short-term savings from an ARM are dwarfed by the consistency and peace of mind a fixed rate provides.

- You are approaching or in retirement. Fixed-income households cannot absorb unexpected payment increases without serious financial strain.

- You are converting from an ARM that is about to adjust. Many homeowners who took out 5/1 ARMs in 2020 at rates around 2.75% are now facing adjustment periods that could push their rates to 6.25% or higher. Refinancing to a fixed rate stops that uncertainty permanently, according to AmeriSave.

- You value budget stability above all else. Fixed payments make it easier to plan for other financial goals like college savings, retirement contributions, or emergency funds.

- You believe interest rates may rise further. With 30-year fixed rates potentially declining toward 5.9% by Q4 2026 according to Fannie Mae, locking in now protects you if that forecast does not hold.

Who Should Consider an ARM Refinance?

An ARM refinance can make financial sense in a narrower set of circumstances.

- You plan to sell within five to seven years. If you are certain you will move or sell before the adjustment period begins, you benefit from a lower initial rate with no exposure to future increases.

- You are a real estate investor or house flipper. Lower early payments improve cash flow on an investment property, and the plan is to sell before the ARM adjusts, as Fortune notes.

- You expect a significant income increase. If you know your earnings will rise substantially within a few years, you can better absorb any upward adjustments when they occur.

- You are a military family or expect a relocation. A defined short-term timeline makes an ARM strategically sound if you know you will be moving before the fixed period ends.

- You are refinancing from a higher fixed rate into a short-term ARM. Some borrowers moving from a 7%-plus fixed rate into a 5/1 ARM are capturing meaningful immediate savings, with a plan to refinance again if rates drop further.

Understanding the Breakeven Point

Before committing to either option, calculate your breakeven point. This is how long it takes for the monthly savings from your new lower rate to exceed the upfront closing costs you paid to refinance.

The formula is straightforward: divide your total closing costs by your monthly savings. If refinancing costs $8,000 and saves you $200 per month, your breakeven is 40 months, or about 3.3 years. If you sell or refinance again before that point, the refinance was not financially beneficial.

For ARM refinancers, the breakeven calculation is more complex. You must also factor in the potential higher payments after the adjustment period begins and whether your lifetime rate caps protect you sufficiently. Most ARMs carry caps such as 2/1/5, meaning the rate can rise 2% at first adjustment, 1% per subsequent adjustment, and no more than 5% over the life of the loan.

| Breakeven SnapshotLoan Amount: $400,000 | Closing Costs: ~$10,000 | Fixed Rate: 6.78% | ARM Intro Rate: 6.34%Monthly savings with ARM intro rate: approx. $125 | Breakeven: ~80 months (6.7 years)If you plan to stay longer than 7 years, the fixed-rate refinance is the stronger choice on a total cost basis. |

The 2026 Rate Context: What It Means for Your Decision

Mortgage rates fell to their lowest point since September 2022 in early 2026, following three consecutive Federal Reserve rate cuts in late 2025. However, rates have climbed back somewhat, with 30-year fixed refinance rates rising to 6.44% in early April before edging higher to 6.78% APR as of April 3, 2026, according to Bankrate.

Fannie Mae projects 30-year rates could decline to around 5.9% by Q4 2026, though the Mortgage Bankers Association forecasts rates holding closer to 6.5% through year-end. The MBA also reported that ARM applications jumped 16% in a single week in October 2025 as borrowers sought to capitalize on the ARM-to-fixed spread, per AmeriSave.

The key takeaway: the spread between fixed and ARM rates today is narrower than historical averages. As NextGen Mortgage points out, when fixed rates are only slightly higher than ARM rates, the traditional rationale for accepting adjustable-rate risk becomes much weaker.

| SUGGESTED IMAGE PLACEMENT #3Insert a line graph here showing 30-year fixed vs. 5/1 ARM average refinance rates from January 2024 through April 2026, illustrating the narrowing spread. Source: Freddie Mac PMMS data. Alt text: ’30-year fixed vs. 5/1 ARM refinance rate trends 2024-2026 showing narrowing spread.’ |

Common Mistakes to Avoid When Choosing Your Refinance Type

- Choosing based on rate alone. A lower ARM rate looks appealing, but always calculate the full cost over your expected time in the home, including what happens after the adjustment period begins.

- Ignoring closing costs. At 2% to 5% of the loan amount, closing costs are a major factor. Refinancing a $400,000 mortgage could cost $8,000 to $20,000 upfront, regardless of whether you choose fixed or ARM.

- Underestimating how long you will stay. Most homeowners who pick an ARM expecting to move within five years end up staying longer than planned. Life changes: job relocations fall through, kids enroll in local schools, housing inventory stays tight.

- Not comparing lenders. ARM pricing varies significantly between lenders. A lower advertised rate may come with a higher margin, meaning steeper post-adjustment payments. Always compare the APR, not just the introductory rate.

- Waiting for the perfect rate. As experts consistently advise: lock in when you find a compelling deal, not the perfect one. Gambling on further rate declines often costs more than it saves.

Frequently Asked Questions

Is a fixed-rate or ARM refinance better in 2026?

For most homeowners, a fixed-rate refinance is the stronger option in 2026. The spread between fixed and ARM rates is historically narrow (around 0.44% to 0.80%), which reduces the benefit of accepting ARM risk. As NextGen Mortgage explains, when fixed rates are only slightly higher than ARM rates, the case for the uncertainty of an adjustable rate weakens considerably. An ARM remains a reasonable choice if you have a firm, short-term exit strategy.

What is the current 5/1 ARM refinance rate?

As of March 24, 2026, the national average 5/1 ARM refinance APR was 6.34%, according to Bankrate’s survey of the nation’s largest lenders. Rates change daily, so always request a personalized quote based on your credit score, equity, and loan amount.

Can I refinance from an ARM back to a fixed-rate mortgage?

Yes. Refinancing from an ARM to a fixed-rate loan is straightforward and works like any other refinance. You will shop lenders, submit documentation, pass an appraisal, and close on a new loan that pays off the old one. Requirements typically include a credit score of at least 620, a debt-to-income ratio below 50%, and at least 20% equity, according to Bankrate.

How do ARM rate caps protect me?

Rate caps limit how much your ARM interest rate can rise, both at each adjustment and over the life of the loan. A common cap structure is 2/1/5: the rate can go up 2% at the first adjustment, 1% at each subsequent adjustment, and no more than 5% above the initial rate over the life of the loan. This means a 5/1 ARM starting at 6.34% could potentially reach a maximum of 11.34% if all caps are hit, which would dramatically increase your monthly payment.

What is a breakeven point in refinancing?

The breakeven point is the number of months it takes for your monthly savings from a lower refinance rate to offset your upfront closing costs. Divide your total closing costs by your monthly payment reduction. If you sell or refinance again before reaching that point, the refinance cost you money overall.

How much does it cost to refinance?

Refinancing typically costs between 2% and 5% of the loan amount, covering appraisal fees, origination fees, title insurance, and other closing costs. On a $400,000 loan, that is $8,000 to $20,000. These costs apply whether you choose a fixed-rate or ARM refinance. Some lenders offer no-closing-cost refinance options, but those savings are usually built into a slightly higher interest rate.

Should I choose a 15-year or 30-year fixed refinance?

A 15-year fixed refinance currently averages around 6.10% APR compared to 6.78% for a 30-year fixed, according to Bankrate. The 15-year saves substantially on total interest but requires higher monthly payments. Choose the 15-year if you can comfortably afford the larger payment and want to pay off your mortgage faster. Opt for the 30-year if you need lower monthly obligations or want to redirect savings toward other financial goals.

The Bottom Line

Fixed-rate or ARM refinance: the right answer is the one that matches your real-life timeline, not just today’s headlines. If you plan to stay in your home beyond seven years and value stability and simplicity, a fixed-rate refinance at today’s rates offers strong, long-term protection. If you have a clear, near-term exit strategy and can tolerate some uncertainty, an ARM’s lower introductory rate may put real money back in your pocket while your plans unfold.

The most important step is running the actual numbers for your specific loan balance, credit profile, and expected time in the home. Rates shift daily, the spread between fixed and ARM products can change week to week, and what looks like a smart move today can look different in six months.

Get personalized quotes from at least three lenders, compare the APR rather than just the stated rate, calculate your breakeven point, and consult with a licensed mortgage professional before signing anything.

| Key TakeawaysFixed-rate refinance rates average 6.78% APR (30-yr) and 6.10% APR (15-yr) as of April 2026.5/1 ARM refinance rates average around 6.34% APR — a spread of roughly 0.44% over 30-yr fixed.About 92% of U.S. mortgage holders choose fixed-rate loans for their payment certainty.A fixed rate is best for long-term owners (7+ years). ARM is best for short-term owners with a clear exit plan.Always calculate your breakeven point and compare at least three lenders before committing. |

Sources and Citations

1. Bankrate – Current Refinance Rates (April 3, 2026)

2. Bankrate – ARM Refinance Rates

3. Bankrate – Should You Refinance ARM Into Fixed Rate?

4. Fortune – Current ARM Mortgage Rates (April 3, 2026)

5. Freddie Mac – Primary Mortgage Market Survey (PMMS)

6. RefiGuide – Best Refinance Mortgage Rates 2026

7. AmeriSave – Should You Refinance Your Mortgage in 2026?

8. Chase – Refinancing an ARM to a Fixed-Rate Mortgage

9. NextGen Mortgage – Fixed Rate vs Adjustable Rate Mortgage 2026